February 7, 2019

Today we share with you a new monthly feature for GAI News — Consultant’s Corner — where our industry experts from HighQuest Consulting provide insight on the latest activities in the ag investing and agtech space. Enjoy!

By Philippe de Lapérouse and Mark Zavodnyik, HighQuest Consulting

The ongoing trade war begun with China last summer has prompted interested parties in the U.S. agricultural sector to question the impact this has already had on the U.S. and global agriculture sector and the implications for the future.

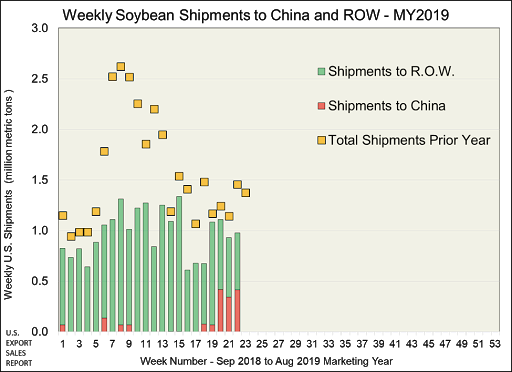

To date, the impact of Chinese tariffs on the U.S. agricultural sector has been significant. For the first five months (Sept. 2018 – Jan. 2019) of the new crop year, U.S. export sales and weekly inspection reports indicate a 38 percent decline in accumulated shipments. The U.S. has exported 21.5 million metric tons of soybeans through the end of January, compared with 34.7 million metric tons for the same period last year.

Since last summer, China, which accounts for more than 60 percent of global soybean trade, has covered its needs almost entirely from Brazil, to avoid the 25 percent duty placed on soybeans imported from the U.S. The U.S. in turn has been supplying soybeans to the rest of the world.

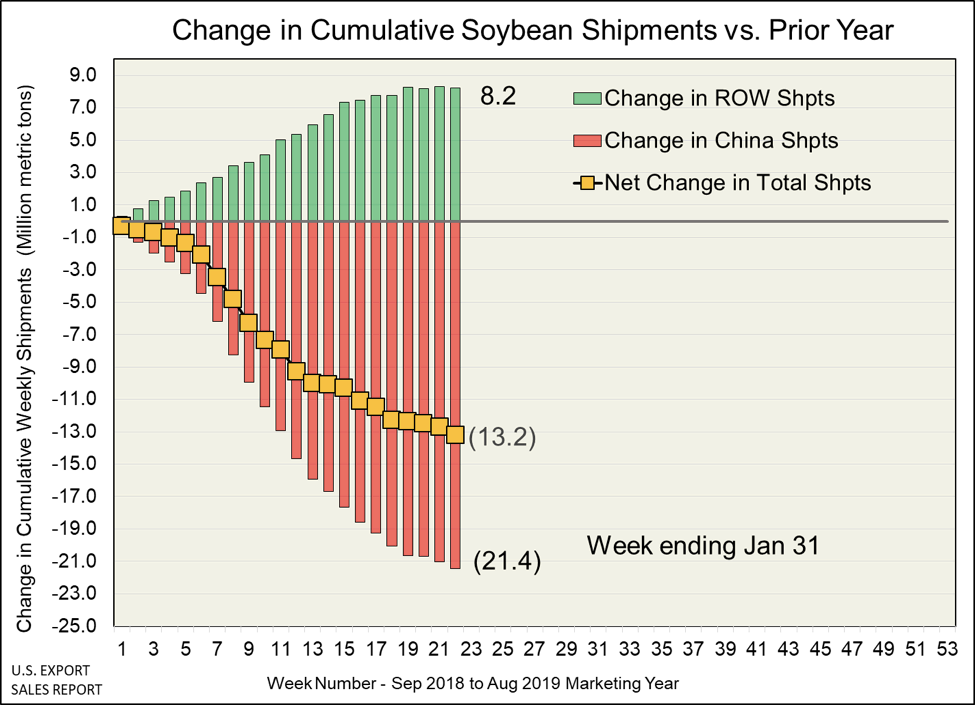

There is not enough soybean import demand in other destinations to fully offset the interruption of demand from China. Through end of January, U.S. shipments to other destinations have increased by only 8.2 million metric tons, compared to last year, while shipments to China have decreased by 21.4 million metric tons. To date, the net decline of U.S. soybean exports amounts to 13.2 million metric tons. In December 2018, the USDA projected marketing year exports of 51.7 million metric tons (1.9 billion bushels), which represents a 6.2 million metric ton decline from the previous year. Thus, for the balance of the 2019 marketing year, U.S. exports will need to achieve a pace that gains on prior year shipments by 7.0 million metric tons just to achieve the USDA’s estimate of marketing year exports.

China has begun purchasing a second round of 5.0 million metric tons of U.S. soybeans, partly to improve the trade negotiating environment, and partly to rebuild stocks. If the U.S. has an opportunity to increase soybean sales to China, other destinations will likely increase their coverage from Brazil. It therefore will be challenging for the U.S. to regain its global share without production problems somewhere else in the world.

While U.S. soybean producers are hard to read with respect to planting intentions for the next crop, some reduction in acreage can be expected. However, after a half dozen years of expanding exports driven by Chinese demand, and price levels supported by seasonally tight pipelines, grower concerns are surprisingly muted, despite the fact that interior basis levels and futures spreads remain weak.

As 2019 begins, this situation raises a number of key issues for stakeholders across the food and agricultural value chain (producers, exports and investors, etc.):

-Are U.S. soybean and corn producers likely to decrease their 2019 planting intentions in order to mitigate future exposure and limit losses?

-How are volumes of soybeans and other soft commodities exported from major origination markets to major destination markets likely to change to make up for the decrease in U.S. exports, and what are the long-term ramifications for trade flows?

-What is the likelihood, assuming that U.S. growers reduce their plantings of soybeans and corn, that the trade war will lead to a build-up of excess stocks of agricultural products in the U.S. as China shifts its purchases to competitive origins such as Brazil and Argentina?

-How is the current trade war likely to affect commodity prices in the medium and longer-term?

-What is the likely impact on the profitability and financial position of U.S. producers over the coming year?

-What impact will this development have on farmland prices in the major U.S. soybean and corn growing regions and will it drive institutional investor appetite for farmland in South America?

-How will the prospect of reduced exports of soybeans and corn in 2019 from the U.S. affect the ability of producers to access credit to finance this year’s crop?

-What is the likelihood the trade war will result in an increase in farm bankruptcies in the U.S. in 2019?

For help examining the ever-changing ag world through consulting and due diligence projects, please contact HighQuest Consulting. www.highquestconsulting.com

ABOUT THE AUTHORS

Philippe de Lapérouse is a managing director at HighQuest Partners, a leading global strategy advisory and consulting firm. HighQuest advises strategic players operating in and financial investors allocating capital to the global food and agricultural value chains on making informed decisions on strategy and resource allocation. Lapérouse chairs the Global AgInvesting conference series. He can be reached in St. Louis at +1 978.887.8800 x365 or via email at pdelaperouse@highquestpartners.com.

Mark Zavodnyik is project manager for HighQuest Consulting. Previously, he was the lead tropical oils trader at AAK USA with responsibility for all palm, palm kernel, and coconut oil sourcing, trading, and risk management for AAK facilities in the United States. Zavodnyik has spoken at a number of industry conferences on the supply/demand factors impacting tropical oil markets, as well as the efforts the industry has undertaken to make palm oil more environmentally sustainable. He can be reached at +1.574.274.3099 or mzavodnyik@highquestpartners.com.

Let GAI News inform your engagement in the agriculture sector.

GAI News provides crucial and timely news and insight to help you stay ahead of critical agricultural trends through free delivery of two weekly newsletters, Ag Investing Weekly and AgTech Intel.