June 29, 2020

Global Food inSecurity: Mega Trends and Post Pandemic Crosscurrents Offer Investment Opportunities in AgFood Tech: Part II. Investment Implications and Opportunities

By Jaleh Daie, Ph.D., chairman/founder of AgFood Tech at the Band of Angels

“All the pests that out of earth arise, the earth itself the antidote supplies.”

— Lithika (400 B.C)

Emerging Themes and Trends

The Ides of March, vintage 2020 upended normalcy, forcing us to adjust to changes including a remote and intensely digital world that had pulled forward five years of digitalization in a mere five weeks. In Part I of this series (see below), I presented the case for a potential global food crisis, accelerated and exacerbated by the COVID-19 pandemic, and observed several immediate and long-term emerging themes that must be addressed to avert a crisis. Each of these themes will bring challenges and opportunities. The emerging themes include: deglobalization and decentralization; breaking supply chains; inflation pressures in consumer staples; demand for regionally grown and distributed food; price sensitivity due to high unemployment; heightened health awareness and demand for fresh, traceable food; and acceleration of bioeconomy and realization of biology as a powerful tool for solutions across all industries that could lead to an easing of regulatory policy to speed up market entry for new innovations. The power of biology has been recognized throughout human history by explorers and observers, reflected in the poetry of Lithika cited above.

In this Part II of the series, I will present my viewpoint on implications for investors and where we may see shifts. There are abundant opportunities and low-hanging fruit both at the upstream (farm) and downstream (food/fork), and along the entire value chain of the AgFood vertical. Some themes will dominate the landscape, becoming the norm. Critically, increased R&D spending in health-related biotechnology will be a great bonanza for AgFood vertical. The advances can be rapidly adopted to the AgFood sector for development of new solutions and applications. We must fully tap into this gift.

In this Part II of the series, I will present my viewpoint on implications for investors and where we may see shifts. There are abundant opportunities and low-hanging fruit both at the upstream (farm) and downstream (food/fork), and along the entire value chain of the AgFood vertical. Some themes will dominate the landscape, becoming the norm. Critically, increased R&D spending in health-related biotechnology will be a great bonanza for AgFood vertical. The advances can be rapidly adopted to the AgFood sector for development of new solutions and applications. We must fully tap into this gift.

Current Investment Landscape

Global investment in 2019 in AgFood was over $20 billion (AgFunder, 2019), nearly 40 times that of 2013 when the first agtech unicorn, Climate Corp, was acquired by Monsanto. Despite major dislocations in the global economy in H1 2020, the food sector was relatively stable. In fact, Q1 investment in food tech saw 25.3 percent uptick.

Expectedly, late-stage valuations crashed, year-on-year, after years of dizzying up-rounds they were already lofty and overdue for a correction. But early stage valuations increased over 50 percent. In the coming months uncertainties may take their toll on when, where, and how risk capital will be deployed. It is too early to pinpoint the fallouts. There are numerous complications at both the macro and micro levels as we witness confusing converges as well as divergences and paradoxes. To complicate matters further, is the flood of cheap money unleashed by central bankers worldwide, encouraging excessive risk-taking already reflected in public markets.

The necessity for resilient food systems has become apparent even to the non-experts, as weakness and vulnerabilities in global food supply chains were laid bare as the pandemic unfolded. Thus, in the mid-long term, AgFood tech will remain a high priority investment choice. As an essential industry, a defensive sector, and a non-correlated asset class, AgFood fits the bill as a solid investment thesis during fraught times. Billionaires have already seen the light. Indeed, for several years, multi-billion- dollar funds backed by luminaries such as Bill Gates, Richard Branson, Peter Theil, Jeff Bezos, and many other large family offices have invested in sustainable agriculture as part of their sustainability and climate goals. In addition, mega multinational corporations such as Microsoft and IBM have entered the fray. Most recently, Yvon Chouinard, the visionary founder of Patagonia, launched a new business venture in food—Provisions. He wrote “I think the only revolution we’re likely to see is in agriculture and I want to be a part of that revolution”. He added “I realize, now more than ever, that the requisite for a thriving business and thriving people are one and the same”. He is joining the billionaires club in seeing the massive potential, something unforeseen just a decade ago.

Post Pandemic Cautious Outlook

Risk and venture capital will favor the afore-mentioned emerging themes. For now, the recent eye-popping valuations will disappear at least for the next couple of years. Investors are in a wait-and-see mode which is expected to last another nine to12 months pending the availability of effective vaccines and therapeutics.

Investors are inclined to fund modest rounds, or are entirely pulling the ripcord from weak companies. Bridge financing and deal-by-deal investments, rather than investing in funds, may become the preferred mode for venture capital and family offices for the foreseeable future. As corporations and institutional investors rethink funding priorities, corporate backed and lower quality accelerators will be forced to pivot or close. Startups across all industries including AgFood are under pressure. Those with a short runway and without a minimum viable product to generate revenue will go dark as funding will go to the strongest and most sustainable. They are lowering expenses and pivoting their business models in a way that would improve their finances and simultaneously improve profit margins for growers. Overall, it is a buyer’s market as discriminating investors preserve cash for follow-on support of their most viable portfolio companies and make selected investments in high priority areas. There would be fewer deals but at more reasonable valuations along with serious triage to redirect cash to the most promising companies in the portfolio. Furthermore, some areas may become more attractive as we grasp the full long-term consequences of the pandemic. Many emerging young investors are losing enthusiasm. Even veteran VCs are re-assessing their next moves. As incurable optimists, and deep believers of technology solutions and innovation, venture capitalists will find ways and spaces to deploy funds with the expectation of attractive returns in the mid-to-long term.

Readjustments are expected at all levels, calling for a re-evaluation of longstanding structures for all players, from government policies to explicitly articulate national food security and health security strategies, to multi-billion family offices, to VCs, angel investors, and founders. Many nations would place high priority on self-reliance, reshoring, and onshore-grown food. Even before the pandemic, most nations were implementing national efforts and investments into local/regional food production. For example, in 2019 Singapore launched the ambitious AgFood strategy of “30 x 30” to produce 30 percent of its food by 2030 and just announced a $14 billion fund to support bio-innovation. China has always viewed food as the core of their national security and will continue to allocate funds to the sector. MENA nations are also on their way to having some degree of self-sufficiency through indoor farming and the purchase of prime farmland. The winners in this race will be the nations that will move with speed and boldness to adapt to new realities.

VCs are expected to wire out fewer funds as the outlook for their own fundraising, especially from corporate LPs, becomes cloudy since corporations are in the preserving cash mode themselves, (first cuts are in the VC arm, along with travel expenses and advertising). In a buyer’s market, investors are less likely to fall all over each other to get into a deal. In a reversal, VCs are once again asserting power with more oversight and frequent pulse taking. Instead of the usual all cash rounds, conditions are imposed to ensure performance: payout for achieving milestones; and pay-to-play to force co-investors to participate; and in rare cases, demanding veto power for their board member(s). According to PitchBook, as early as May 2020, nearly 7,200 U.S. startups were on the verge of “have to raise” or very close to it. With founders facing the loss of a dream, many are sitting up and listening and when forced to raise, they accept down rounds and bridge financing. Founders are adapting by preserving cash, cutting expenses (adieu free lunch and great parties), especially on staff, travel, and office space as work at home becomes the norm.

After all is said and done, the fact remains that opportunities are plenty along the entire AgFood vertical which is only in its third inning.

In today’s fraught and uncertain conditions, the old play books are being edited and some parts entirely rewritten. For example, the aggressive growth at any cost model was well accepted and indeed touted by many VCs. That practice is now coming into question and scrutiny. There is a shift to focus on unit economics, sustainability, and path to profitability, over blitz scaling. Family offices, while enjoying a greater degree of independence and freedom may view changes in the VC attitudes as clues. However, the magical potion in the brew is the almost no cost money sloshing around, which may bring the frenzied pace back sooner than later. The notion of never let a crisis go to waste is already revived taking advantage of the torrent of cheap money—reminiscent of post 2000 and 2008 market turmoil when the strongest survived. Indeed, many internet/digital superstars were born after the tech crash of 2000 and the 2008 financial crisis.

Investment Implications

Despite a significant decline in venture investing in Q1 2020, and thousands of thinly-funded startups facing dissolution, investment in the AgFood sector should remain relatively attractive. As one of the least digitized industries, agriculture offers the greatest potential. In fact, all classic analog industries such as agriculture, food, real estate, and insurance may get new attention as investors will fund vertical SaaS models as these industries become more digital.

Plentiful pain points along the AgFood value chain present great investment opportunities. First, an unexpected bonus is awaiting us—a rush of investments in health-related biotech and health supply chain logistics will result in superb advances in health care preparedness. The AgFood community must exploit this gift of low-hanging fruit by quickly adopting such advances. How efficiently and cleverly we adopt such technologies will form a new narrative in food and nutrition security. Returns will be best on what farmers really need: less expensive farm inputs and savings in water, chemicals, and labor, such as cost-saving and sustainable inputs that can be adopted in the 10-30-60 model (product used on 10 percent of crops in the first year, 30 percent and 60 percent in later years). However, the bar may be high because of a longer adaptation time due to a potentially long tail cycle and budget cuts in R&D.

With high unemployment, consumers will be price sensitive, and health conscious. This awareness undergirds the new trend of food for health and food as medicine based on clean, traceable, and functional foods and ingredients. New investment opportunities will emerge from social distancing and the growth in direct-to-consumer transactions. We are facing a paradox of food shortage and waste due to supply chain/logistics disruptions for which supply chain management and assurance platforms are needed to close the gaps. There will be a rise in the use of robotics and automation along the entire supply chain to respond to labor shortages and to minimize human points of contact and touchless transactions. The need for production reshoring will create opportunities for vertical and indoor farming systems to respond to higher demand for regional/local products. Inflationary pressures and supply chain breaks in the meat sector are resulting in higher demand for alternative proteins including insects, plant-based, and cultured protein. Ingredients makers would do well by producing healthy products, as consumers use food choices for wellness. Investment in biotech, especially for farm input materials and for desirable traits via synthetic biology and gene editing via CRISPR technology offer great opportunities. Governments are likely to ease regulations regarding genetic modification and gene editing to shorten the product to market cycles as well as gaining new markets and competitive edge.

Competition among exporting countries for market share will increase as nations place a high priority on sufficient onshore-grown food. The situation calls for a re-evaluation of long standing structures for all players. Even before the pandemic, most nations were directing national efforts and investments into local/regional food production. Nations can get into the front ranks of a new bioeconomy to not only diversify their economy, and in the case of exporters, to diversify their markets. Those with advanced biotech and digital economies can up their game in food and agtech quickly and without difficulty. Supportive policies can speed up the regulatory clearance process to quickly advance to market critical needs technologies, such as biotechnology, and to improve their competitive edge by creating a national food and nutrition security strategy as a core part of the national security portfolio, which will ensure a resilient food system.

There is no shortage of prospects and potential gains in the burgeoning digital agriculture. The time to sow the seeds is now.

Note: An Asia-Australia focused version of this was published in an essay by Jaleh Daie in Disruptive Asia. Vol.4, 2020

ABOUT THE AUTHOR:

Dr. Jaleh Daie is a global thought leader and partner at Aurora Equity investing alongside family offices in early stage startups. She is board director and Women in Technology International Hall of Famer. Concurrently, she is chairman/founder of AgFood Tech at the Band of Angels. She started her career at UW-Madison and Rutgers University where she achieved the rank of full professor in six years, was first woman chair of an agronomy department, founder and chief executive of an interdisciplinary center, and senior science advisor to the president. Simultaneously, she managed three administrative operations while running an externally funded research program resulting in over 100 peer reviewed papers in top journals, was elected as president of the national Association for Women in Science and first woman chairman of the Council of Scientific Society Presidents, among other roles. Dr. Daie has served as head of STEM at the David and Lucile Packard Foundation and the administration of three presidents. She serves on several boards and is recipient of numerous awards, including a Congressional Citation for her advocacy of women and minorities.

Dr. Jaleh Daie is a global thought leader and partner at Aurora Equity investing alongside family offices in early stage startups. She is board director and Women in Technology International Hall of Famer. Concurrently, she is chairman/founder of AgFood Tech at the Band of Angels. She started her career at UW-Madison and Rutgers University where she achieved the rank of full professor in six years, was first woman chair of an agronomy department, founder and chief executive of an interdisciplinary center, and senior science advisor to the president. Simultaneously, she managed three administrative operations while running an externally funded research program resulting in over 100 peer reviewed papers in top journals, was elected as president of the national Association for Women in Science and first woman chairman of the Council of Scientific Society Presidents, among other roles. Dr. Daie has served as head of STEM at the David and Lucile Packard Foundation and the administration of three presidents. She serves on several boards and is recipient of numerous awards, including a Congressional Citation for her advocacy of women and minorities.

*All views, data, opinions and declarations expressed are solely those of the author(s) and not of Global AgInvesting, GAI News, GAI Gazette, or parent company HighQuest Group.

___________________________

Global Food inSecurity: Mega Trends and Post Pandemic Crosscurrents Offer Investment Opportunities in AgFood Tech: Part I. The Bioeconomy Era: Is a Biology Generation Born with Convergence of Digital Age and Bio Century?

By Jaleh Daie, Ph.D., chairman/founder of AgFood Tech at the Band of Angels

“Nothing lasts forever. Everything is a change waiting to happen.”

The ides of March, vintage 2020 was a moment in history that brought home the notion of back to basics like no other time in modern history: without food, health, and shelter, economic metrics need not apply.

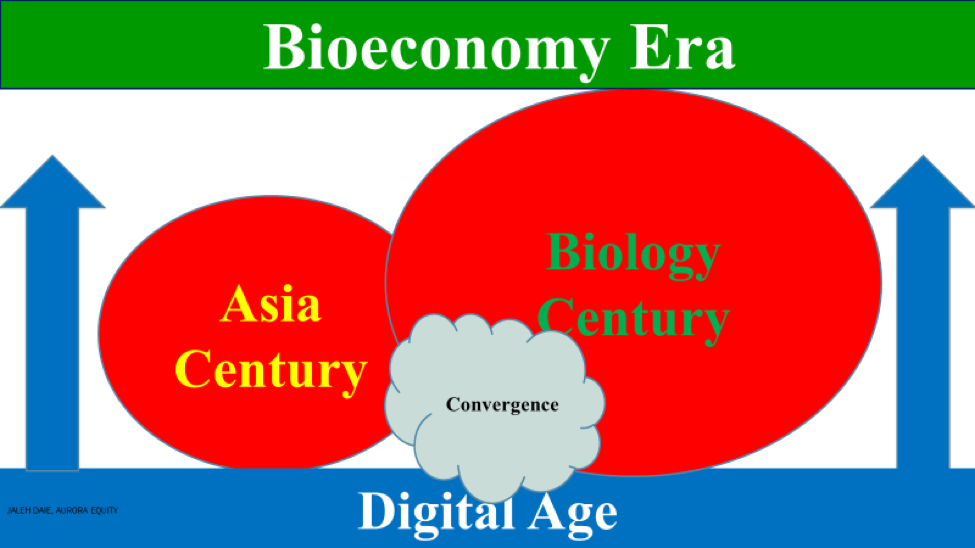

In this two-part series, I will present a case that at this post pandemic juncture, along with global mega trends such as rapid growth in world population, and middle-class expansion in Asia, we must exploit the convergence of digital age with biology century and Asia century to invest in sustainable and resilient food systems. The backdrop of a bioeconomy offers great opportunities for investment across the broad AgFood innovation spectrum to help farmers and consumers, and to mitigate environmental impact, all bolstered by a new generation of biologists (Gen B).

Part I. The Bioeconomy Era: Is a Biology Generation Born with Convergence of Digital Age and Bio Century?

State of Play

The world population will reach 10 billion by 2050, more than half of which is Asian, requiring 70 percent increase in food production. As Asia rises, the middle class in Asia Pacific alone will be five times that of Europe and 10 times North America. Food security dynamics in Asia are complex. While Asia is home to nearly two-thirds of the world’s hungry, the rapid rise in the middle class has put enormous pressure on protein demand. To meet such demand, production must increase by more than 50 percent by 2030.

Global food security challenges are so vexing because of the dichotomy of hunger and obesity. Nearly 700 million are hungry, including 260 million on the brink of starvation, yet more than two billion are overweight with poor metabolic health due to malnourishment. Therefore, to truly address global food security, we must place equal emphasis on nutrition to remedy another pandemic—chronic illnesses and the associated metabolic ailments. The recent United Nations Global Report on Food Crisis warns that “the world is at risk of widespread famines of ‘biblical proportions.’” It is becoming increasingly clear that we cannot continue inefficient past practices, and that the only way to avert this tragedy is through transformative innovation in food production and distribution.

In many developing economies, especially in greater Asia, food and agriculture value chains have been major pillars of GDP, employment, and social stability. Even before the COVID-19 pandemic, the world had been facing food and nutrition challenges. Post pandemic the system is facing additional stress, forcing both food importers and exporters to rethink their short- and long-term food security plans with full consideration of the fact that decades of globalization have resulted in centralized production and distribution systems, creating fragilities in the supply chains.

Moreover, food has always been a national security concern. Increasingly, food and agriculture are considered core foci of national security. For example, the EU Commission just released its Farm to Fork and Biodiversity strategy aiming to create a more “robust, secure and sustainable food system”. China has allocated large sums of funds to innovation in food and agriculture, and Singapore has announced their 30×30 Strategy to produce 30 percent of their food needs by 2030. Clearly, national security considerations are going beyond trade and availability issues to self-reliance and maintaining sustainable, regionally produced food. This priority is almost foreordained since agriculture is one of the least digitized industries and is ripe with ample opportunities and low hanging fruit for a digital roadmap to a food secure future. Thankfully, appetite for innovation in critical need areas such as health, food, and agriculture are strong, and the true and tested mantra of disrupt or be disrupted persists.

It is too early to know how long the current displacements will last, what fallouts will impact food availability patterns, and how food importers and exporters might realign with shifting supply and demand patterns. To achieve the massive goal of global food security, international coordination and cooperation are essential. Yet, geopolitical tensions are rising with bifurcation of alignments among G7 and G20 nations at a time when ensuring the integrity and cohesiveness of the global health and food supplies and their respective industries is essential. The knee-jerk reaction has been one of “you are with us or not.” For example, China has been extending carrots to Europe, Africa, and others in its sphere of influence with health supplies, but tensions are rising as it faces a backlash for how it handled information sharing about the COVID-19 outbreak

The Convergence of Biology Century and Asia Century in the Digital Age

The convergence of digital and biology ushered in and is unleashing the bioeconomy era. According to a McKinsey report (Bio-Revolution, May 2020) over 60 percent of all global physical input could be made using biological means, using currently available technologies. A legacy of COVID-19 is a sure acceleration of this mega trend. The rise of the Asian middle class has had an enormous impact on food, especially animal protein demand.

The pandemic upended normalcy, especially how, where, and what food we buy and eat, going back to the basics of food, health, and shelter in a span of a few weeks. The behavior changes and rapid pace of adoption of new ways of life have been nothing short of astonishing. The great acceleration of remote-machines-robotics-digital pulled forward five years of digitalization in a mere five weeks, resulting in several new trends, most of which will be with us for the foreseeable future, and likely permanently.

As we work to meet the immediate food challenges, and address shifting consumption patterns, consideration must be given to whether sustainability, climate change, and sustainable development goals will remain focal points as they were before the pandemic when there was consensus on global issues such as climate change, reflecting a sense of the greater good (for all of us, everywhere). In just a few weeks we seem to have swung to a me, here mindset. Widespread hoarding of supplies, including by nations, breaking supply chains, and asset devaluation offer clues. However, this is neither the time nor a reason to ignore important macro issues. Agriculture is a major contributor of greenhouse gas emissions and thus must become sustainable and central to addressing climate change—killing two birds with one stone.

Post Pandemic Fall-Outs and Emerging Trends

The post pandemic represents many disharmonies- macro and micro crosscurrents are vexing and fraught with dichotomies, paradoxes, bifurcations, and divergences, making prediction of how and where things will ultimately settle difficult. Many SMEs are facing financial hardship or closure. Big is getting bigger, as big box retailers are increasingly selling non-essentials leading to acceleration of SME closures.

We may be entering an era of back to basics in which economic expansion may take a back seat to securing food supplies and protecting public health. More importantly, the winners in this race will be those who can rapidly translate these challenges into pragmatic and positive outcomes to maintain their competitive edge. Against this backdrop of major challenges and a fraught post- COVID-19 world, several themes are unfolding, each of which offer great investment opportunities:

— Deglobalization. Decades of globalization and centralization in pursuit of efficiency and profit have laid bare the weaknesses along the entire food value chain. Global food supply chains are breaking as growers and labor-intensive food processing centers face labor shortages. There is a new model of just-in-case vs the current just-in-time one. The weaknesses point to the need for more distributed systems of the supply chain to prevent a single weak link to cause a domino effect. When, where, and how such disruptions result in food scarcity and inflationary pressures is not clear but could exacerbate global food insecurity.

— Local and regional production, reshoring, and onshoring are getting due attention as nations aim to become more self-reliant using indoor and vertical farming, among other things. At the micro level we are witnessing a flight to suburbia in search of “earth”, revival of victory gardens, and urban farming around big cities.

— High unemployment. A prolonged period of high employment is setting in, requiring new ways to ensure accessibility of affordable healthy food for all. High unemployment would lower demand in discretionary spending and disruptions in food supplies would mean inflationary pressure for essential consumer staples. No one would win under such a scenario (for example, while cattle prices are falling, meat retail prices are rocketing up and meat packers cannot profit from the situation). This bifurcation will test the resilience of our systems. Despite such turbulence, I am confident that innovation in AgFood tech along with appropriate policies can address such emerging themes.

— Homing, home cooking, ecommerce, direct to consumer (DTC) and home delivery of food, especially locally grown are taking hold. While consumers’ exodus to online had already happened, food was the outlier with modest moves. Not any longer.

— Heightened health awareness is leading to discerning consumers demanding clean, healthy food at reasonable prices, delivered to them in convenient, hygienic, and mostly touchless ways. Automation and robotics will provide solutions and could see rapid expansion in use. Robots are expected to become commonplace.

— Food for health and food as medicine are taking new meaning and are becoming mainstream, from nice to do to must do. Genetic advances are enabling personalized nutrition leading to customized diets as wellness tools. Functional ingredients are finding their way into more foods as consumers rethink their food intake choices.

— Biologists have known for over 20 years that the 21st century belonged to biology. Now, the public at large is fully aware of the unbound power of biology–both destructive and its miraculous ability to solve troubling problems in health, agriculture, food, fiber, energy, and materials. There is talk of AgFoodShot—a serious national commitment in pursuit of biological discoveries, inventions, and applications.

— New biotech and synthetic biology tools such as gene editing are solving longstanding problems. Many products are already in the market and a full pipeline is awaiting entry. Governments are likely to ease regulations to fast track commercialization of new biology-based critical needs and products.

A Path Forward: Harnessing the Power of Biology

As we navigate this brave new world of uncertainties, a decades-long generational shift is unfolding with the emergence of a consumer- and health-centric era. The post-pandemic world is fraught with vulnerabilities in the global food supply chains, potential shortages, widespread hunger, and the dichotomy of inflation in necessities and deflation in luxuries. In the short-to-medium term it is hard to know how various crosscurrents will play out. In the long run, it is certain that human ingenuity will overcome the challenges to build a resilient food system. We will innovate our way out of this crisis too, as humanity has done over millennia.

This new era of bioeconomy, digital agriculture, and food, and biotech is here to stay. It is unfolding in the most astonishing and rewarding ways. My realistic hope, and indeed, expectation, is that this crisis will spawn a global Sputnik 2.0: the emergence of a biotech generation – Gen B – much as the launch of the Sputnik spaceship kicked the baby boomer generation into choosing science and technology careers in large numbers during the century of physics and chemistry. Gen B is the new Gen Z.

Despite the pains and tragedy of loss of life, hunger, and poverty, one thing is clear – the human ingenuity will, at some point and fashion, help resolve the current uncertainties and challenges. The winners will understand, embrace, and exploit the enormous momentum in the bioeconomy and will profit from it. Governments and nations must facilitate and help advance the cause of ensuring healthy, affordable food through innovation in sustainable agriculture. They can sharpen their competitive edge by heeding the opportunities presented by the bioeconomy and ceasing the dawn of the century of biology.

NOTE: An Asia/Australia-focused version of this article appeared in an essay by Jaleh Daie in Disruptive Asia, Volume 4, May 2020.

ABOUT THE AUTHOR

Dr. Jaleh Daie is a global thought leader and partner at Aurora Equity investing alongside family offices in early stage startups. She is board director and Women in Technology International Hall of Famer. Concurrently, she is chairman/founder of AgFood Tech at the Band of Angels. She started her career at UW-Madison and Rutgers University where she achieved the rank of full professor in six years, was first woman chair of an agronomy department, founder and chief executive of an interdisciplinary center, and senior science advisor to the president. Simultaneously, she managed three administrative operations while running an externally funded research program resulting in over 100 peer reviewed papers in top journals, was elected as president of the national Association for Women in Science and first woman chairman of the Council of Scientific Society Presidents, among other roles. Dr. Daie has served as head of STEM at the David and Lucile Packard Foundation and the administration of three presidents. She serves on several boards and is recipient of numerous awards, including a Congressional Citation for her advocacy of women and minorities.

*All views, data, opinions and declarations expressed are solely those of the author(s) and not of Global AgInvesting, GAI News, GAI Gazette, or parent company HighQuest Group.

Let GAI News inform your engagement in the agriculture sector.

GAI News provides crucial and timely news and insight to help you stay ahead of critical agricultural trends through free delivery of two weekly newsletters, Ag Investing Weekly and AgTech Intel.