By Weiyi Zhang, Ph.D., Senior Agricultural Economist, Manulife Investment Management

The financial performance of farmland and agricultural investments is driven by both market specific factors and developments in the global macroeconomic environment. The recent dramatic changes in the U.S. economy, including rising inflation and interest rates, are already impacting farmland operations and income. The financial performance of farmland and agricultural investments has shown incredible resilience during previous recessions and periods of economic turbulence. This resilience will be tested as headwinds build, with economic growth slowing and the risk of a near-term recession on the rise.

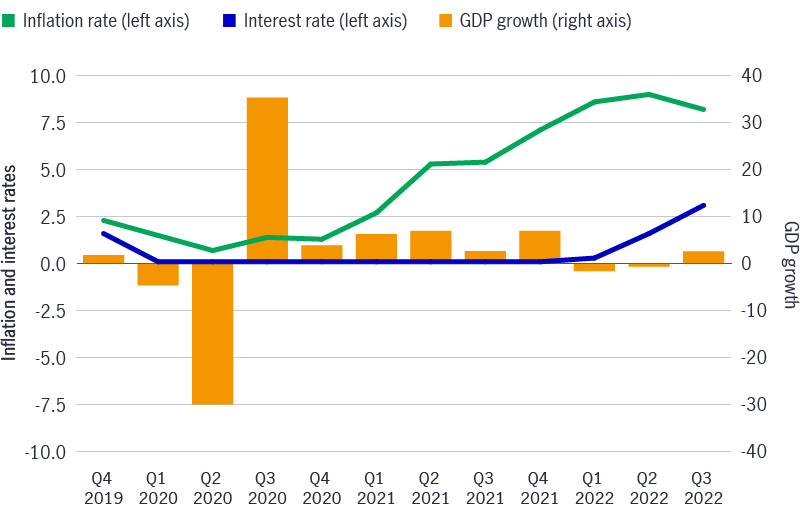

Evolving macroeconomic landscapes over the past three years

Inflation rate, interest rate, and GDP growth in the U.S. from Q4 2019 to Q3 2022 (%)

Source: Inflation rates: U.S. Bureau of Labor Statistics, Consumer Price Index for All Urban Consumers: All items in U.S. city average, November 22, 2022. Interest rates: Board of Governors of the Federal Reserve System (U.S.), Federal Funds Effective Rate, November 22, 2022. GDP growth: U.S. Bureau of Economic Analysis, real gross domestic product, November 22, 2022. The GDP growth rate is calculated as the annualized quarter-over-quarter rate of change in real GDP.

Farm products registered price gains as inflation rates rose

Demand for goods and services rebounded quickly following the pandemic-induced recession in early 2020, aided by a series of monetary and fiscal measures undertaken to inject liquidity into the system and ultimately support the economy. The juxtaposition of rapidly rising demand and pandemic-induced supply chain constraints led to surging inflation beginning in early 2021. Within agriculture specifically, U.S. farmland markets responded quickly to the changes in the inflationary environment. The rapid recovery in demand for farm products placed strong upward pressure on prices for agricultural crops, after the short-lived declines seen during the pandemic induced recession. Farm product prices posted double-digit percentage gains in both 2020/2021 and 2021/2022 marketing years, more than offsetting the initial 11 percent drop in the price level seen during March–April 2020. Several factors contributed to the enhanced demand prospects for major U.S. agricultural, including consumers’ increasing interest in healthier diets that boosted domestic fruit and tree nut consumption, reopening local economies that reinvigorated fuel consumption and lifted the outlook for ethanal and by extension corn, and strong export demand.

Farm product prices posted strong gains in 2020/2021 and 2021/2022 marketing years

Percentage changes in monthly producer price index for U.S. farm products

Source: U.S. Bureau of Labor Statistics, Producer Price Index series ID WPU01, not seasonally adjusted, as of October 2022.

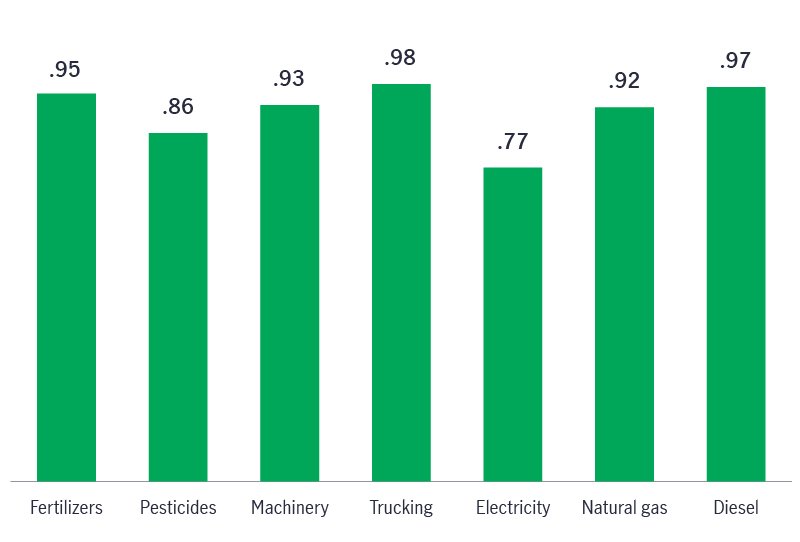

Agricultural production costs pushed up due to high inflation rates

Increasing inflationary pressures in major input cost categories have had a direct impact on farm operations, and most farm-related cost categories have shown increases for over two years. From the trough seen during the first months of the pandemic in 2020 to the peak levels of 2022, major input costs, including fuel and energy, machinery, chemicals, and fertilizers, surged, with increases ranging from 30 percent for machinery to 120 percent for natural gas costs.

Agricultural production faced significantly higher costs

Percentage changes in PPI categories from trough to peak during 1/20 to 10/22

Source: U.S. Bureau of Labor Statistics, Producer Price Index series, not seasonally adjusted, as of October 2022. PPI IDs: fertilizer WPU0651, pesticides WPU0653, machinery WPU1114, trucking WPU3012, electricity WPU0543, natural gas WPU0553.

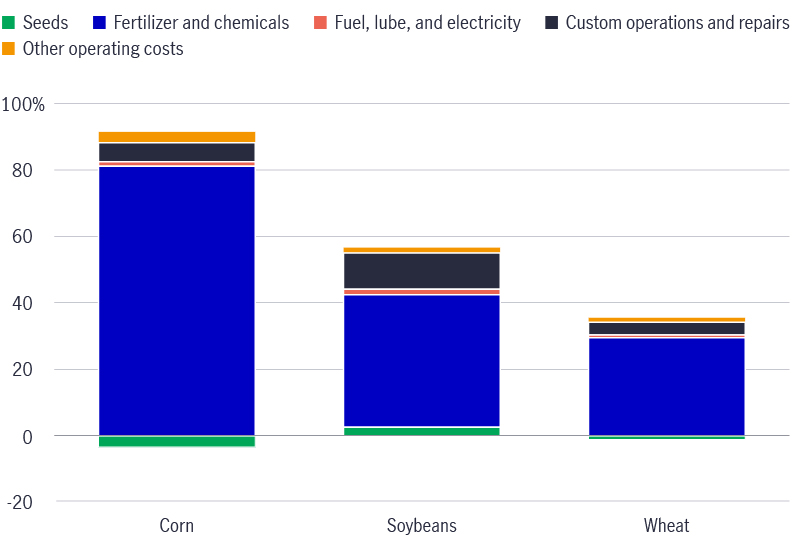

Due to differing cost structures, the impact of higher inflation on operating costs varied by crop type, and while surging prices for fertilizer and other chemical inputs accounted for most of the rising operating costs of major U.S. row crops in percentage terms, the dollar impact of these increases varied. Specifically, the effects of the dramatic rise in fertilizer and chemical costs were significant for corn, soybeans, and wheat, with a respective 92 percent, 71 percent, and 84 percent of the per-acre operating cost increases attributed to higher fertilizer costs from 2020/2021 to 2022/2023 . However, this masks the disparity of the impact between different crops. U.S. corn farmers are forecast to pay $81/acre more for fertilizers in 2022/2023 relative to the average fertilizer costs of 2020/2021. In comparison, U.S. soybean and wheat growers are forecast to pay $40/acre and $29/acre more for fertilizers and other chemicals over the same period. Per-acre cost impact also influenced farmers’ planting decisions: In 2022, U.S. farmers planted 4.6 million fewer acres of corn relative to a year ago despite high corn prices, while soybean acreage gained a quarter million acres due to the relatively smaller impact from rising fertilizer costs. Overall, combined planted acres of corn, soybeans, and wheat declined by 5.4 million acres in 2022 compared with 2021, illustrating the direct impact that rapidly rising costs had on farmers’ planting decisions.

Cost impact varies by crop and cost structure

Changes in per-acre operating costs ($US) during 2022/2023 compared with 2020/2021 for U.S. corn, soybeans, and wheat

Source: USDA Economic Research Service using Agricultural Resource Management Survey data and other sources, as of June 2022.

Farm profits rise as revenue growth outpaced cost hikes in 2022

For over two years, agricultural product prices have largely kept pace with increasing input costs, measured by the correlation between monthly price indexes of farm products and major input cost categories, including energy, chemical inputs, machinery, and transportation. This positive correlation statistically demonstrates crop prices’ capability to keep pace with rising input costs and has allowed farmers to at least partially offset rampant increases in input costs, providing operators and investors some relief within an inflationary environment. This capability was demonstrated through the expected increase in farm profits forecast by the USDA in the face of rapidly rising input costs during 2021 to 2022, with net farm income forecast to increase 5.2 percent ($7.3 billion) year-over-year.[1]

Strong crop prices could help offset higher input costs

Correlation between farm products price index and cost price indexes during 1/20–10/22

Source: U.S. Bureau of Labor Statistics, MIMTA research, as of October 2022.

The evolution of the relationship between interest rates and agricultural investment returns and farmland values

Interest rates are another macroeconomic factor affecting agricultural investments. U.S. interest rates have experienced several hikes in 2022, with additional increased expected heading into 2023. Meanwhile, U.S. farmland values have increased significantly in the past two years. According to the USDA’s annual surveys, average U.S. farmland values increased by 7.0 percent and 12.4 percent in 2021 and 2022.[1] Despite this strong appreciation in farmland values, investors have become more cautious as the U.S. Federal Reserve (Fed) continues to raise interest rates in an attempt to control persistently elevated inflation. Looking back, the appreciation in farmland values has been supported by the relatively low interest-rate environment witnessed since the Great Financial Crisis (GFC) and by strong farmland returns. Looking forward, expectations for crop prices, and the pace and duration of further interest-rate increases, are expected to be key determinants of farmland values.

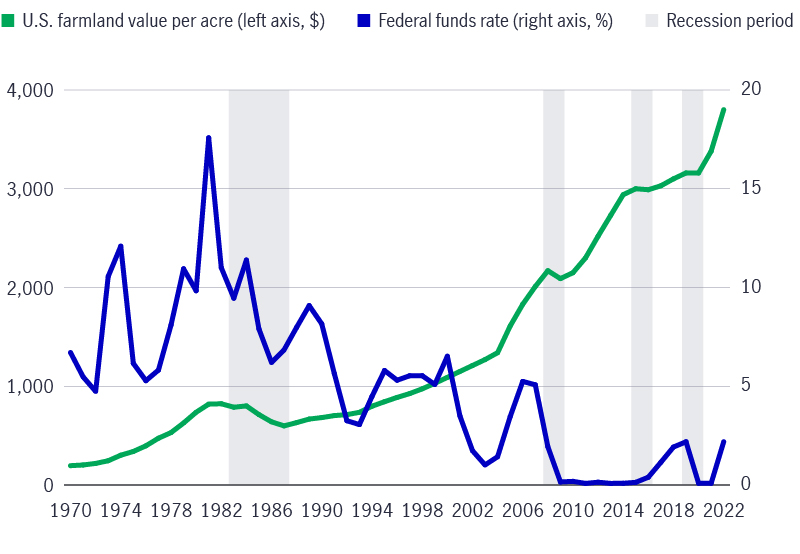

Land values have increased steadily, while interest rates have trended lower and been more volatile

U.S. farmland values, represented by average U.S. farm real estate values as calculated in the USDA’s annual surveys, have shown incredible growth and resilience for more than five decades.[2] U.S. farmland values have expanded at an average annual rate of 5.8 percent since 1970, only declining seven times on a year-over-year basis. When market conditions are robust and positive—supported by rising crop prices, demand and other sources of income—U.S. farmland has appreciated at an average rate of 7.8 percent per year. On the other hand, farmland values have also displayed relatively modest declines during periods of weaker market fundamentals (as indicated by the shaded areas in the chart below). During these periods, land values only retreated at an average annual rate of 5.1 percent per year.

Farmland values have risen alongside generally declining interest rates for over five decades

Federal fund rate (%/year) vs. U.S. average farmland value ($/acre) from 1970 to 2022

Source: USDA NASS, as of October 2022; FRED, Federal Reserve Bank of St. Louis, as of October 2022. Federal funds rates are annual average rates. Shaded areas indicate periods of farmland value depreciation.

Interest rates have a complex relationship with farmland appreciation

In general, an increase in interest rates may create downward pressure on asset prices. This negative relationship is illustrated by the negative correlation (-0.7) between U.S. average farmland values and the federal fund rates seen from 1970 to 2022. However, the relationship between interest rates and farmland values is more complex and differs from that of other traditional financial asset classes, including stocks and bonds. Changes in farmland values tend to lag interest-rate changes and are more heavily influenced by broader agricultural market factors such as rising per capita income and the supply-demand balance. Therefore, the recent surge in interest rates alone is highly unlikely to result in imminent farmland value depreciation as current values appear to be in line with returns and interest rates.

The historically dynamic correlation between farmland value and interest rates

The overall negative long-term correlation between farmland value and interest rates masks a more dynamic pattern. When viewed on a rolling 10-year basis, farmland values exhibited a positive correlation with interest rate as they trended slowly higher from the 1970s through mid-1990s. This rolling 10-year correlation turned largely negative beginning in the mid-1990s, as interest rates eased steadily lower through 2017. As the Fed attempted to normalize interest rates and began raising rates again in 2017, farmland values continued to rise on positive agriculture market fundamentals and the correlation once again turned positive.

The historically dynamic correlation between interest rates and farmland values

Trailing 10-year correlation between USDA farmland values and interest rates from 1970 to 2022

Source: USDA NASS, as of October 2022; FRED, Federal Reserve bank of St. Louis, as of October 2022; MIMTA Research, November 1, 2022. 10-year correlations are calculated as the correlation between farmland values and federal funds rate in the trailing 10-year periods.

Farmland returns are a key driver of farmland value

Like other asset classes, farmland derives its value as a function of discounted future returns. Expected future farmland returns can be calculated by the estimated future income generated from the underlying land. For leased farmland, which is a prevalent management type for annual row cropland used by institutional investors, cash rents can be used as a proxy for future income. Higher cash rents typically lead to higher farmland values, and data from the state of Illinois (one of the more active and mature U.S. farmland markets) shows the exceptionally strong positive correlation (0.98) between farmland values and cash rents. Between 1970 and 2022, the average farmland value in Illinois increased at an average rate of 5.7 percent per year, while average cash rents increased by 3.7 percent per year. Over the past two years, Illinois’ average cash rents accelerated upward and increased 7.0 percent on a per-acre basis from $227 in 2021 to $243 in 2022. Meanwhile, average farmland values appreciated at an even faster rate of 12.6 percent, from $7,900 per acre to $8,900 per acre over the same period. Cash rents are usually driven by expectations for near-term commodity prices and the availability of government-sponsored financial support programs, but tend to lag the changes in commodity prices slightly. Prices of major agricultural crops have retreated from historical highs entering the new marketing year yet are forecast to remain at elevated levels relative to historical averages, offsetting higher operating costs and maintaining modest upward pressure on cash rents in 2023. This upward momentum in cash rents is expected to carry over into 2023 and could provide additional support for further land value appreciation in the near term.

Farmland values trend well with farm income historically

Illinois farmland value ($/acre) and cash rent ($/acre) from 1970 to 2022

Source: USDA NASS, as of October 2022

Agriculture proves its resilience during economically uncertain times

As investors brace for the potential of an economic recession in the next 18 months, historical analysis of the performance of agriculture and farmland in other economically uncertain periods can provide additional insight for future market performance. Farmland has generated positive income returns during the majority of the past five-plus decades and once again, using Illinois as a proxy for the broader agriculture sector, farm rents on Illinois farmland have provided stable and growing income returns for its owners, with rents declining on a year-over-year basis in only 11 of the 52 years between 1970 and 2022. Diving deeper, farm rents decreased by 4 percent per year during the 11 down years on average compared with the 6 percent per-year growth seen during the remaining 41 years. This demonstrates the sticky behavior of farm cash rents that have largely increased along with positive market developments, and displayed resistance to downward pressures during periods of weaker and deteriorating market conditions for more than five decades.

Farm income returns exhibit historical resilience

Illinois farm cash rents year-over-year change (%)

Source: USDA NASS, as of October 2022. Shaded areas represent recession periods, defined by the Federal Reserve Bank of St. Louis, as of October 2022.

Institutional farmland investments have weathered economic downturns well, providing positive returns for over three decades

Specific to institutional farmland investments, the National Council of Real Estate Investment Fiduciaries (NCREIF) Farmland Index (NFI) was created in 1991 to measure the investment performance of privately owned and managed U.S. farmland properties and is widely considered to be an appropriate proxy for U.S. farmland investment returns. Since the NFI’s inception in 1991, U.S. farmland has exhibited resilient performance, generating positive returns throughout each of the four recessions over the past 30 years. Income returns held relatively steady, while appreciation provided periodical augmentation for total return performance. And, agricultural investments provided investors with consistent performance during separate periods, delivering 8.4 percent per year during the pre-dot-com years (1991–1999), 14.4 percent per year leading into the GFC (2000–2008), and 9.8 percent per year during the protracted recovery period post-GFC (2009–2021).

Institutional farmland investments have fended off recessionary pressures historically

NCREIF Farmland Index total return (%)

Source: NCREIF, as of October 2022. Shaded areas represent recession periods, defined by the Federal Reserve Bank of St. Louis, as of October 2022.

Agriculture-specific market factors have been the dominant influence on farmland returns

The impact of high inflation and rising interest rates has historically been outweighed by farmland market fundamentals. For example, from the 1970s to the early 1980s, farmland returns generated positive incomes and appreciation alongside rising interest rates and high inflation. During this period, despite higher interest rates, agricultural market performance was driven by burgeoning international demand for U.S. crops. In the early to mid-1980s, interest rates declined rapidly from their historic highs as inflation rates moderated. However, farmland values declined despite the easing monetary environment due to the lagged impact from the record rise in interest rates into the early 1980s that ultimately resulted in a significant farm crisis. Fast-forward to 2015 and onward, as the U.S. economy was in the middle of a prolonged and slow economic recovery characterized by under-target inflation rates, the Fed’s monetary policy normalization strategy resulted in a gradual increase in interest rates, while farmland values were experiencing a period of mild and positive growth. Finally, in 2021 and 2022, farmland values expanded at a robust rate of 9.7 percent per year, as the Fed pivoted toward a much more hawkish monetary policy position and began ratcheting interest rates higher to combat rampant inflation. Above all, these instances demonstrate the outsized influence of underlying market fundamentals compared to changes in interest rates, but the lagged impact of interest rates on farmland values should not be overlooked.

The positive outlook for agriculture is driving steady farmland returns amid an evolving macroeconomic landscape

The positive momentum from the increasing farmland returns of the past two years is expected to be maintained in the near term. However, returns could be weighed down by macroeconomic headwinds, including sustained high inflation and interest rates, and the increasing likelihood of a near-term economic recession. The extent of these macroeconomic headwinds will be a key determinant of future farmland returns. Going forward, downward pressure on farmland returns could occur if: 1) a global economic recession significantly lowers demand for farm products and consequently weighs on income returns over an extended period, or 2) inflation and interest rates continue to increase or remain elevated. For farm income returns, while major crop prices are forecast to moderate from current highs as shipping bottlenecks dissipate and global markets regain balance, prices are projected to remain moderately elevated relative to history. Tight market conditions are expected to persist, making the sector exceptionally sensitive to potential shocks, and supporting a positive income outlook for farmland investments. These positive market dynamics make sustained downside risks for farmland returns less likely. On the other hand, while the duration and magnitude of current interest-rate hikes remain unclear, the likelihood of an extended period of historically high interest rates reminiscent of the 1980s is low, which should help limit the probability of mounting downward pressure on farmland values from higher interest rates. In addition, investors’ increasing emphasis on nonfinancial goals, such as the environmental and social features and impacts of their investments, creates a new tier for farmland demand. As agricultural production integrates technological innovations, agriculture can play a key role as a natural climate solution, providing additional opportunities for farmland investors and injecting new enthusiasm for farmland moving forward.

In conclusion, while near-term downward pressure from the current high inflation and interest-rate environment exists amid the increasing likelihood of a global recession, solid agriculture-specific market fundamentals are anticipated to outweigh these pressures and continue to support the long-term appreciation of values and returns on farmland investments. Therefore, we believe agriculture remains uniquely positioned to traverse the near-term cyclicality, volatility, and uncertainty prevalent in today’s markets.

SOURCES:

[1] USDA ERS, https://www.ers.usda.gov/topics/farm-economy/farm-sector-income-finances/highlights-from-the-farm-income-forecast/, September 1, 2022.

[2] USDA NASS QuickStats, as of October 2022.

ABOUT THE AUTHOR

Weiyi Zhang, Ph.D. is a senior agricultural economist with Manulife Investment Management. In this role, he conducts economic research to support the firm’s business and agricultural investment decisions, and is directly involved in farmland transactional due diligence and initiating new investment strategies and concepts. In addition, he is responsible for the global agricultural economic, financial, and statistical analytical efforts, including commodity price forecasting, portfolio analysis, and authoring thought leadership publications. Previously, Zhang was the senior natural resource economist, where he supported economic research and analysis for the group’s timberland and farmland business sectors. He holds a bachelor of science in agricultural and applied economics, a master of forest resources (M.F.R.), and a Ph.D. in forest finance and economics.

Weiyi Zhang, Ph.D. is a senior agricultural economist with Manulife Investment Management. In this role, he conducts economic research to support the firm’s business and agricultural investment decisions, and is directly involved in farmland transactional due diligence and initiating new investment strategies and concepts. In addition, he is responsible for the global agricultural economic, financial, and statistical analytical efforts, including commodity price forecasting, portfolio analysis, and authoring thought leadership publications. Previously, Zhang was the senior natural resource economist, where he supported economic research and analysis for the group’s timberland and farmland business sectors. He holds a bachelor of science in agricultural and applied economics, a master of forest resources (M.F.R.), and a Ph.D. in forest finance and economics.

Important disclosures

A widespread health crisis such as a global pandemic could cause substantial market volatility, exchange-trading suspensions and closures, and affect portfolio performance. For example, the novel coronavirus disease (COVID-19) has resulted in significant disruptions to global business activity. The impact of a health crisis and other epidemics and pandemics that may arise in the future could affect the global economy in ways that cannot necessarily be foreseen at the present time. A health crisis may exacerbate other preexisting political, social, and economic risks. Any such impact could adversely affect the portfolio’s performance, resulting in losses to your investment.

Investing involves risks, including the potential loss of principal. Financial markets are volatile and can fluctuate significantly in response to company, industry, political, regulatory, market, or economic developments. These risks are magnified for investments made in emerging markets. Currency risk is the risk that fluctuations in exchange rates may adversely affect the value of a portfolio’s investments.

The information provided does not take into account the suitability, investment objectives, financial situation, or particular needs of any specific person. You should consider the suitability of any type of investment for your circumstances and, if necessary, seek professional advice.

This material is intended for the exclusive use of recipients in jurisdictions who are allowed to receive the material under their applicable law. The opinions expressed are those of the author(s) and are subject to change without notice. Our investment teams may hold different views and make different investment decisions. These opinions may not necessarily reflect the views of Manulife Investment Management or its affiliates. The information and/or analysis contained in this material has been compiled or arrived at from sources believed to be reliable, but Manulife Investment Management does not make any representation as to their accuracy, correctness, usefulness, or completeness and does not accept liability for any loss arising from the use of the information and/or analysis contained. The information in this material may contain projections or other forward-looking statements regarding future events, targets, management discipline, or other expectations, and is only current as of the date indicated. The information in this document, including statements concerning financial market trends, are based on current market conditions, which will fluctuate and may be superseded by subsequent market events or for other reasons. Manulife Investment Management disclaims any responsibility to update such information.

Neither Manulife Investment Management or its affiliates, nor any of their directors, officers or employees shall assume any liability or responsibility for any direct or indirect loss or damage or any other consequence of any person acting or not acting in reliance on the information contained here. All overviews and commentary are intended to be general in nature and for current interest. While helpful, these overviews are no substitute for professional tax, investment or legal advice. Clients should seek professional advice for their particular situation. Neither Manulife, Manulife Investment Management, nor any of their affiliates or representatives is providing tax, investment or legal advice. This material was prepared solely for informational purposes, does not constitute a recommendation, professional advice, an offer or an invitation by or on behalf of Manulife Investment Management to any person to buy or sell any security or adopt any investment strategy, and is no indication of trading intent in any fund or account managed by Manulife Investment Management. No investment strategy or risk management technique can guarantee returns or eliminate risk in any market environment. Diversification or asset allocation does not guarantee a profit or protect against the risk of loss in any market. Unless otherwise specified, all data is sourced from Manulife Investment Management. Past performance does not guarantee future results.

Manulife Investment Management

Manulife Investment Management is the global wealth and asset management segment of Manulife Financial Corporation. We draw on more than a century of financial stewardship to partner with clients across our institutional, retail, and retirement businesses globally. Our specialist approach to money management includes the highly differentiated strategies of our fixed-income, specialized equity, multi-asset solutions, and private markets teams—along with access to specialized, unaffiliated asset managers from around the world through our multimanager model.

This material has not been reviewed by, is not registered with any securities or other regulatory authority, and may, where appropriate, be distributed by the following Manulife entities in their respective jurisdictions. Additional information about Manulife Investment Management may be found at manulifeim.com/institutional.

Australia: Manulife Investment Management Timberland and Agriculture (Australasia) Pty Ltd, Manulife Investment Management (Hong Kong) Limited. Canada: Manulife Investment Management Limited, Manulife Investment Management Distributors Inc., Manulife Investment Management (North America) Limited, Manulife Investment Management Private Markets (Canada) Corp. China: Manulife Overseas Investment Fund Management (Shanghai) Limited Company. European Economic Area Manulife Investment Management (Ireland) Ltd. which is authorised and regulated by the Central Bank of Ireland Hong Kong: Manulife Investment Management (Hong Kong) Limited. Indonesia: PT Manulife Aset Manajemen Indonesia. Japan: Manulife Investment Management (Japan) Limited. Malaysia: Manulife Investment Management (M) Berhad 200801033087 (834424-U) Philippines: Manulife Investment Management and Trust Corporation. Singapore: Manulife Investment Management (Singapore) Pte. Ltd. (Company Registration No. 200709952G) South Korea: Manulife Investment Management (Hong Kong) Limited. Switzerland: Manulife IM (Switzerland) LLC. Taiwan: Manulife Investment Management (Taiwan) Co. Ltd. United Kingdom: Manulife Investment Management (Europe) Ltd. which is authorised and regulated by the Financial Conduct Authority United States: John Hancock Investment Management LLC, Manulife Investment Management (US) LLC, Manulife Investment Management Private Markets (US) LLC and Manulife Investment Management Timberland and Agriculture Inc. Vietnam: Manulife Investment Fund Management (Vietnam) Company Limited.

Manulife, Manulife Investment Management, Stylized M Design, and Manulife Investment Management & Stylized M Design are trademarks of The Manufacturers Life Insurance Company and are used by it, and by its affiliates under license.