By Michelle Pelletier Marshall, Global AgInvesting Media

The 14th annual Global AgInvesting, held April 4-6, 2022, back in NYC for the first time since the pandemic, was very well-received and attended by nearly 800 in the sector, from institutional investors to family office managers to innovators and agribusinesses. Topics covered included managing water risk, measuring farmland investment performance, the outlook for tech integration, opportunities in natural capital, and much more. Here are some sound bites from a few of the presentations from Global AgInvesting 2022.

Geopolitical Macro Drivers Impacting Global Agriculture Supply Chains

With speaker Deborah Perkins, Global Head of Food & Agribusiness, ING Bank

Deborah Perkins, global head of food & agribusiness with ING Bank since 2017, hails from Australia, and works with her team to finance food and agribusiness companies across the globe. With stints at Rabobank and the State Bank of Western Australia, Perkins now calls Dallas, Texas, home. She covered the effects of market dynamics on the food and ag sector. Here’s a snippet of what she had to say:

“We are going to have a population of 9.7 billion by 2050 and 10 billion by 2100 so we are going to have more people to feed which is going to continue to drive the demand for food, and mean that us as the ag sector need to look for ways to continue increasing production. There’s also income growth occurring in developing countries which means that they’re moving away from a subsistence diet, and they want to consume more protein, more dairy, more processed foods.”

And food prices, she noted, are at the highest level seen since 2011, up 28 percent globally in 2021. And while, Perkins noted, “we might blame it [higher food prices] on Ukraine, we might blame it on the pandemic. But these things were going up prior to that, which gives the indication that food prices really are a reflection of the run up that we’ve seen in commodity prices.” Perkins discussed some of the factors causing the increase in food production/availability across the supply chain:

And food prices, she noted, are at the highest level seen since 2011, up 28 percent globally in 2021. And while, Perkins noted, “we might blame it [higher food prices] on Ukraine, we might blame it on the pandemic. But these things were going up prior to that, which gives the indication that food prices really are a reflection of the run up that we’ve seen in commodity prices.” Perkins discussed some of the factors causing the increase in food production/availability across the supply chain:

Transportation – Approximately 80 percent of global trade occurs via ocean trade and containers. During COVID, supply chain disruptions occurred when workers were not able to get to the ports to unload products and trucks were idled from making deliveries. Containers ended up being stranded in ports, resulting in container shortages and mismatched options for containers.

Labor – “It doesn’t matter who I talk to or where they are in the world or what industry they’re in, everybody is dealing with challenges with labor,” said Perkins. “So as part of your investment strategy, that could be something to keep in mind as well. Where are the workers that you’re going to need for your property going to come from? Do you need to provide housing in addition to some of the other strategies and perks needed to retain employees?”

Perkins noted that the flip side of labor shortages was increased adoption of technology and automation use in ag. “This in turn will change the skill set of the people that we need – you’re going to have more engineers, more people that can actually operate and deal with the issues that might arise as a result of automation.”

Energy prices – The global increase in fuel passes through into a direct increase in the cost of producing food. But, noted Perkins, there are other indirect implications of that as well, such as that energy is one of the key inputs of fertilizer. So if energy prices are going up, fertilizer prices are going up too, exacerbated by the Ukraine, Russia situation because Russia is a key producer of fertilizers.

“Yes, commodity prices are really, really high, but if the input costs are also going up exponentially, that means that the margins for the farmers will not be as high as what they would be if they were just getting higher prices,” said Perkins. “And that will lead to various implications for their investment strategies.”

Climate – Droughts, floods, other extreme weather conditions, not to mention the issue of carbon capturing, have plagued the globe recently, and all of this has an impact on plantings, production, and supply.

Creating Value and Impact for Investors with Organic Farming

With speaker Craig Wichner, Managing Partner, Farmland LP

With 30 years’ experience in building companies and building management, Craig Wichner founded Farmland LP in 2009. Farmland LP is a leading investment fund that generates returns by converting conventional commercial farmland to sustainable. The company manages over 15,000 acres and more than $200 million in assets where it leases two-thirds of its farmland and directly farms the rest. Here’s some notable info from Wichner’s presentation:

“There is $3.3 trillion of farmland in the U.S., which has the same economic value as all of the office buildings in the U.S., and 54 percent of U.S. farmland is leased, so it is essentially commercial real estate,” said Wichner. “The key for us is that you can go from a commodity crop to a higher value crop, thereby increasing the cash flow generated from that land, then you create value.”

And doing this is certainly attainable given the fact that in the U.S. spending on organic food has been growing at double digit rates for the past 25 years, yet only 1 percent of U.S. farmland (3.5 million acres) is certified organic, noted Wichner, adding that the organic food market is 100 percent constrained by supply.

And doing this is certainly attainable given the fact that in the U.S. spending on organic food has been growing at double digit rates for the past 25 years, yet only 1 percent of U.S. farmland (3.5 million acres) is certified organic, noted Wichner, adding that the organic food market is 100 percent constrained by supply.

Wichner spoke of moving away from monocropping, or growing the same crop year-after-year on the same soil, which is not sustainable and has negative impacts on soil health, pollinator habitat, and more.

“We look at it a different way, we say ‘hey, what’s the best use for that farmland?’ and then map out the 10-year sustainable ag rotation and bring in the best farmers for that particular rotation,” said Wichner of the Farmland LP process of converting to sustainable farming. “We get the land certified organic, by investing in infrastructure, drip irrigation, large farm equipment, value-added facilities, and we convert the land to higher value crops, which gives us access to the 50-200 percent price premiums.”

Why Net Zero Changes Everything

With speaker Dave Chen Chief Executive Officer, Equilibrium

Equilibrium CEO David Chen, leads the company in investing and operating sustainably driven real assets portfolios in agriculture, food, and distributed waste-water-energy infrastructure, for institutional investors. Chen has held executive roles at OVP Venture Partners, GeoTrust, McKinsey & Company, and The Ascent Group. Here are the highlights from Chen’s presentation:

“Agriculture is ground zero for both climate risk and sustainability constraints.”

“One of the things I would like to point out, though, that hasn’t been talked a lot about is volatility. And that is there’s a tremendous amount of attention that’s being paid to climate trends as they affect agriculture, and as I like to say, it’s hard to move a piece of land. So if the climate is changing, you’re stuck with it.”

“No one’s paid attention to volatility and weather as it relates to asset pricing and asset performance and agriculture. We’ve got seasonal volatility. And you know that that’s the number one driver of ag performance and ag quality, which obviously has market consequences of price, scarcity, the ability to pay, and regulation.”

“If you take a step back, what’s affected almost every single major market sector over the last decade, from telecom to banking to media, is technology disruption in every sector, the symmetry between the customer and the business. If you think about the symmetry that’s happening in our own sector between the farmer, the consumer, and our intermediary, the retailer, the QSR, you can start to see the symmetry of information has changed everything. And then there’s decarbonization and energy transformation.”

“If you take a step back, what’s affected almost every single major market sector over the last decade, from telecom to banking to media, is technology disruption in every sector, the symmetry between the customer and the business. If you think about the symmetry that’s happening in our own sector between the farmer, the consumer, and our intermediary, the retailer, the QSR, you can start to see the symmetry of information has changed everything. And then there’s decarbonization and energy transformation.”

“I would say that this conversation about Net Zero and climate has gone from mañana to now as people realize that this Net Zero thing is not going away.”

“And remember, Net Zero is about zero emissions for your business. I want you to really embrace what that means for your business. It means as much emissions as my business creates and causes, I have to sequester or reduce or eliminate to zero. Think about what that really means.”

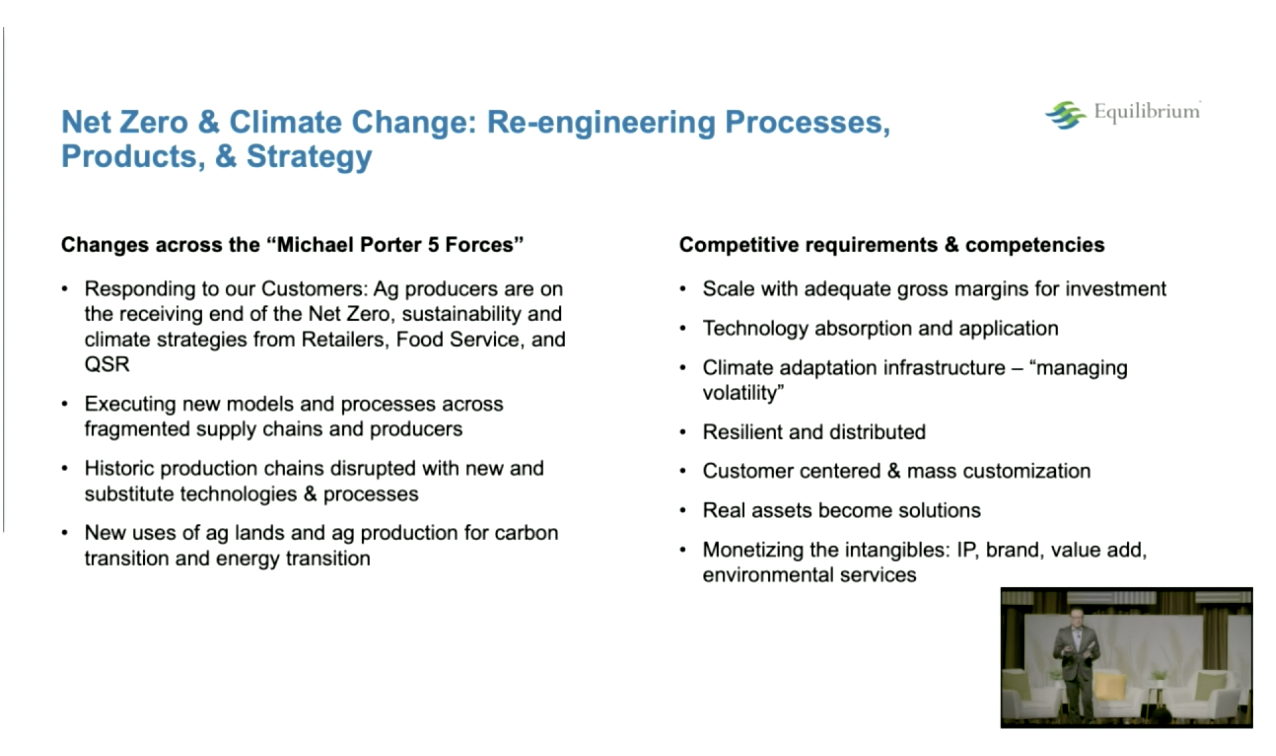

“What’s happening is that most of the businesses that we invest in are beholden to someone else, whether it’s the retailer, the QSR – those are names like Walmart, Amazon. And they’re going to make Net Zero by the way, and they’re going to make it our problem. So that means that ag producers are on the receiving end of Net Zero strategies, and sustainability and climate strategies from a retailer or food service and our QSR. I would actually add that there’s one more – our major leading LPs. We’re executing and we have another challenge here in this industry. And that is that we’re executing these bold, great re-engineering challenges in highly fragmented supply chains.”

“What are the outcomes of this? We’re seeing an entirely new class of investors entering ag because they see this disruptive opportunity taking place. We have new investors who are questioning the real implications of what these changes mean. There’s a whole set of vocabulary questions that are being asked of us now in terms of what we’re investing in. And it’s happened before in the ag sector, the scaling of wind, solar, bio, ethanol, biodiesel, even fracking. And we’re happy seeing that happen again, in areas like controlled environment, agriculture, alternative proteins, next generation genetics, next generation green fuels, renewable natural gas, green hydrogen, and green ammonia. And you’ll see a wave of new strategies that could be recapitalized as carbon transition infrastructure, and climate adaptation infrastructure.”

“So one of the things that’s happened with the Net Zero implication is fitting in our strategies and our innovative capacity as the ag investor into the strategies that best fit into the Net Zero.”

Learn more about the speakers and presentations from Global AgInvesting 2022 here, or join us for our next event, Global AgInvesting Asia, October 20-21, 2022, in Tokyo.

– Michelle Pelletier Marshall is contributing editor and author for HighQuest Partners’ GAI News and Unconventional Ag, and managing editor for its WIA Today blog. Additionally, she is the company’s Senior PR/Media Manager. She can be reached at marshall@highquestpartners.com.

– Michelle Pelletier Marshall is contributing editor and author for HighQuest Partners’ GAI News and Unconventional Ag, and managing editor for its WIA Today blog. Additionally, she is the company’s Senior PR/Media Manager. She can be reached at marshall@highquestpartners.com.

*The content put forth by Global AgInvesting News and its parent company HighQuest Partners is intended to be used and must be used for informational purposes only. All information or other material herein is not to be construed as legal, tax, investment, financial, or other advice. Global AgInvesting and HighQuest Partners are not a fiduciary in any manner, and the reader assumes the sole responsibility of evaluating the merits and risks associated with the use of any information or other content on this site.